Venturing forth – the push and pull of early stage valuations

Company valuation is difficult enough in public markets but for early stage companies, lack of track record and profits means that valuation rests mostly on what someone is prepared to pay. Apple’s valuation crystallises every fraction of a second during stock market hours when a trade is booked, but private company valuation crystallises about annually, when investors hand over cash to company management and become shareholders. Company value at this moment equates to funds raised divided by the percentage of the company sold to new investors. This sounds obvious but it means management needs to convince investors that the cash handed over is appropriate to the business needs and will get the business to its next, higher valuation milestone, and that will determine dilution. Our friends at Go4Venture help us “do the math”.

Fundamentals do matter, of course. A company needs to be forecasting at least high double digit growth in revenues in its early years with a plan to reach profitability but beyond that Go4Venture provides us with a widely used rule of thumb:

- The capital raised needs to take the business to its next agreed milestone in the coming 12 months and then fund a further 6 months to prepare and raise the next round;

- Dilution should be around 30% for a normal company but lower (say 20%) for a “hot” issuer and higher (perhaps 40%) for an unfashionable business or at a weak stage of the cycle.

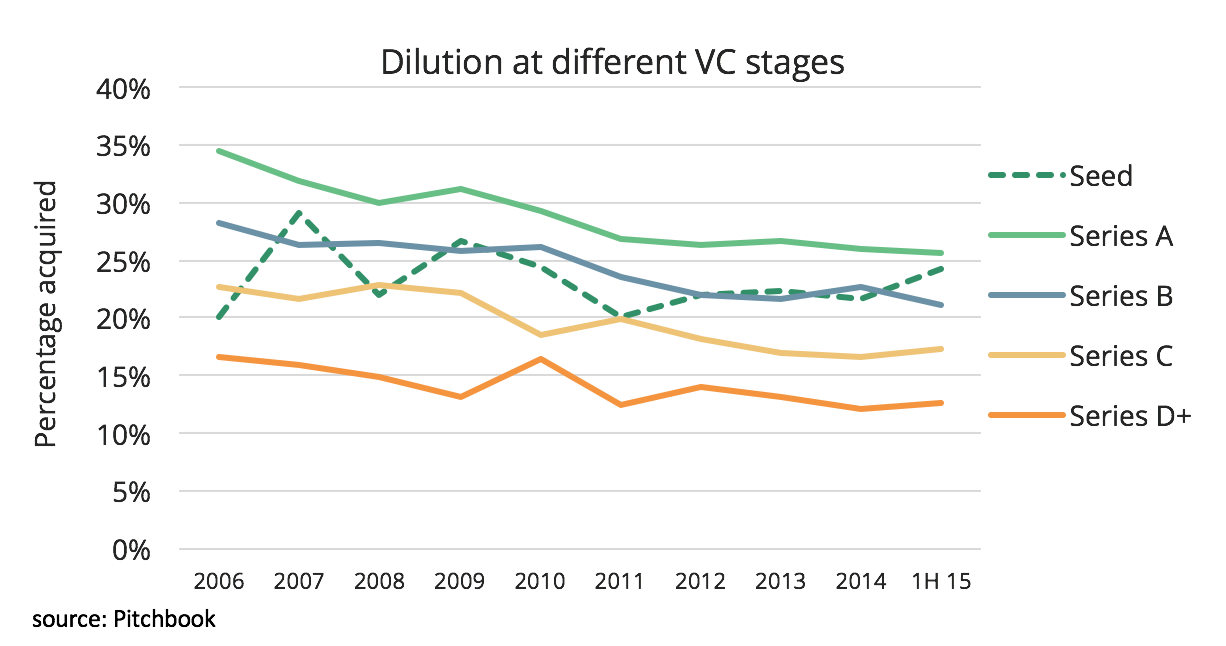

Then, a pre-money valuation can be derived from the funds raised (N) and the dilution percentage (D) as (N/D)-N. The data below shows median valuation and dilution for VC funding deals in the US in 1H15 and was collated by Pitchbook.com.

Source: Go4Venture, Pitchbook.com, Oakhall

In practice, many seed rounds are carried out under the VC radar by angels or friends and family. This explains why the Pitchbook seed round valuation looks high to us and we would expect the majority of seed fundings to be carried out in the $1-5m range.

Milestones matter

For a technology company, Go4Venture notes that typical milestones at each round could be:

- Seed round: take an idea to a prototype

- Series A: develop a revenue model in one country from a working prototype

- Series B: expand a working revenue model in one country to new regions

- Series C: full international expansion

- Series D and later: move into a new segment on the back of a successful technology platform

The valuations and the timing of rounds will depend on the type of company. Internet B2C businesses can scale internationally much more quickly, which often compresses the time frame for Series A/B and can boost valuations. Similarly, in an upswing there is a tendency to reduce execution precautions and companies may seek finance to either outspend competition (e.g. Uber), gain first mover advantage in all countries (e.g. Rocket Internet) or accelerate growth through acquisitions (e.g. Fab.com). Management need to ensure the milestone is deliverable with the funds raised to enable future rounds.

Balancing dilution

If we assume three venture rounds followed by an IPO, 30% dilution is about the “right” level to ensure that the founders of the business remain motivated. Much higher and their stake in the business at exit becomes too small, much lower and it may be difficult to raise the required funds at each stage of the business’s development.

Source: Go4Venture

There is no right valuation

Early stage company execs often ask us what their business is worth and while we can attack the question in many ways and give scientific sounding answers, in truth there is no right valuation and anyone who tells you there is is probably pitching for business with you to raise funds. As an old banker colleague put it, pitching to win business is poetry, doing the deal is prose. Oakhall helps companies size their markets, model their businesses, and prepare their fund-raising pitches.